EIA: Increasing U.S. gasoline inventories are reducing gasoline prices

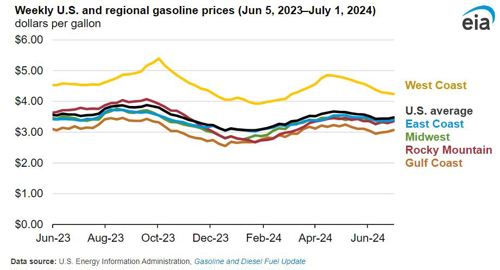

Weekly U.S. average gasoline prices have declined $0.19/gallon (gal) since the 2024 high on April 22, falling to $3.48/gal on July 1, $0.05/gal less than the price a year ago. Increasing gasoline inventories, relatively weak demand and oil prices below recent peaks are all contributing to falling gasoline prices, according to the U.S. Energy Information Administration (EIA).

Increasing gasoline inventories, subdued demand. Increasing gasoline inventories have put downward pressure on gasoline prices. On April 19, U.S. gasoline inventories were 226.7 MMbbl, 8.5 MMbbl less than the previous five-year (2019–2023) average. Between April 19 and June 21 (the most recent week available), U.S. gasoline inventories increased by 7.1 MMbbl to 233.9 MMbbl, essentially equal to the previous five-year average. The increase has been driven by unseasonably large inventory growth in the East Coast, which increased by 4.1 MMbbl over the same period. The large inventory growth in the East Coast offset seasonal gasoline inventory declines in the Midwest and Rocky Mountains.

Inventories on the East Coast increased, in part, because of more gasoline imports, which follow seasonal trends. Historically, more than 80% of U.S. imports of gasoline enter through the East Coast. Gasoline imports into the East Coast hit a 2024 low of 381,000 bpd the week of April 5 but increased after that and averaged 630,000 bpd the week of June 21, a 65% increase. Data from Vortexa Analytics indicate that most of this increase is driven by increased imports of gasoline from Europe.

Inventories are increasing because of higher refinery runs at the same time that demand for gasoline has been subdued. U.S. gross refinery inputs using a four-week rolling average increased from 14.9 MMbpd the week of February 23—the lowest in 2024 to date—to 17.4 MMbpd the week of June 14. Runs declined slightly the week of June 21, averaging 17.3 MMbpd, but remained more than runs at the same time in 2022 and 2023. On the East Coast, refinery runs have been above 2022 and 2023 for most of the year. So far in 2024, our proxy for U.S. gasoline consumption, product supplied, is down about 1% from 2023 levels and below the 2015 to 2019 range.

Crude oil prices. Although they have increased through most of June, crude oil prices, the largest contributor to the price of gasoline, generally declined between early April and early June. The price of Dated Brent crude oil, an international benchmark, reached a 2024 high of $93/bbl on April 12 before falling to $76/bbl on June 5. Crude oil prices in early April were driven by heightened geopolitical risk related to ships transiting the Red Sea and general elevated tensions in the Middle East, along with an OPEC+ announcement to extend production cuts. Since then, however, oil markets have generally adapted to longer shipping routes that avoid the Red Sea, and OPEC announced potential increases in crude oil supply. Crude oil prices remain below the highs seen in April, and as of July 1, the price of Dated Brent was $88/bbl.

Northeast Gasoline Supply Reserve. In addition, the closure of the Northeast Gasoline Supply Reserve (NGSR) will add a modest amount of gasoline supply to East Coast markets. On May 21, 2024, the U.S. Department of Energy’s Office of Petroleum Reserves announced a solicitation for the sale of 1 MMbbl of gasoline from the NGSR. However, the total volume of the sale is relatively small compared with regional gasoline consumption, which averaged 3.2 MMbpd of gasoline in June 2023. Because of the relatively small size of the NGSR, any effects on prices are difficult to distinguish from larger market trends.

Comments